Full Accounting

— Who Must Maintain and How

Full accounting (complete double-entry bookkeeping) is mandatory for certain companies — primarily limited liability companies and public enterprises. But what exactly does full accounting involve? What are the components? When must books be closed? What are the deadlines for financial reporting? As a chartered auditor, I guide you through every element and requirement.

Who Is Required to Maintain Full Accounting?

Full accounting is mandatory for:

- Limited Liability Companies (Sp. z o.o.) — all sizes

- Joint-Stock Companies (S.A.) — all sizes

- Limited Partnerships (Sp. komandytowa) — with corporation partners

- Banks and financial institutions

- Insurance companies

- Large entrepreneurs: Sole proprietors and partnerships with revenue exceeding 2,500,000 EUR (10,646,500 PLN) in prior year

Voluntary full accounting:

Any entrepreneur not required by law can voluntarily adopt full accounting. This is often advantageous for:

- Entrepreneurs seeking bank financing

- Companies planning to grow beyond limits

- Those wanting detailed financial visibility

Elements of Full Accounting

1. Transaction Journal (Dziennik)

Chronological record of all business transactions with:

- Transaction date

- Description

- Debit and credit accounts

- Amounts

2. General Ledger (Księga Główna)

Summary of all accounts, showing balance before and after each transaction.

3. Subsidiary Ledgers

- Inventory ledger: Stock movements and valuations

- Sales ledger: Customer invoices and settlements

- Purchases ledger: Supplier invoices and payments

- Fixed asset register: Depreciation schedules

4. Chart of Accounts (Plan Kont)

Structured list of all accounts used in the company. Must include:

- Asset accounts (0–2)

- Equity and liability accounts (3–5)

- Revenue accounts (4)

- Cost accounts (5)

- Financial result accounts (8)

5. Financial Statements

- Balance Sheet: Assets, liabilities, equity

- Income Statement: Revenues, costs, profit/loss

- Additional Information: Notes to accounts, explanations

Accounting Year Closing Procedures

Key deadlines:

- February 28/29: Last day for transaction entries

- March 31: Books must be closed (complete)

- 30–45 days after approval: Financial statements filed with Business Registry (KRS)

- April 30: Tax declarations (PIT/CIT) due

Closing procedure:

- Calculate account balances

- Prepare trial balance (agreement check)

- Post adjusting entries (depreciation, accruals)

- Prepare financial statements

- Obtain management board approval

- General meeting/shareholders approval (if required)

- File with Business Registry

Components of Financial Statements

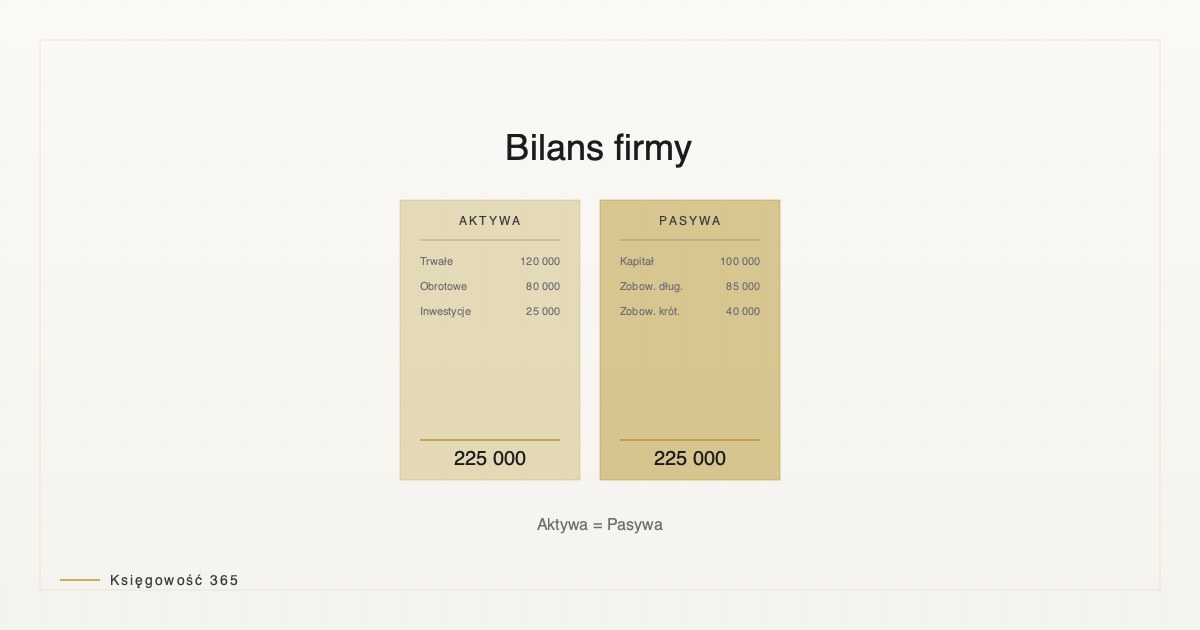

Balance Sheet (Bilans):

Shows financial position at year-end:

- Assets: Current (cash, receivables), fixed (equipment, real estate)

- Liabilities: Current (payables, short-term debt), long-term

- Equity: Share capital, retained earnings, profit/loss

Income Statement (Rachunek zysków i strat):

Shows financial performance for the year:

- Revenue from sales

- Cost of goods sold

- Operating expenses

- Financial income/costs

- Profit before and after tax

Notes to Accounts (Informacja dodatkowa):

Explanatory information including:

- Accounting principles

- Major asset compositions

- Debt structures

- Related-party transactions

- Contingent liabilities

Audit Requirements

Who must have an audit:

- All joint-stock companies (S.A.)

- Limited companies with employees 50+ (all sizes exceeding defined thresholds)

- Companies with assets exceeding 2.5M EUR or revenue 5M EUR

Audit scope:

- Verification of accounting entries

- Assessment of financial statement compliance with law

- Evaluation of internal controls

- Issuance of audit opinion (unqualified, qualified, or adverse)

Record Retention Requirements

All accounting documents and books must be retained for:

- 5 years — invoices, payment documents, ledgers

- 6 years — correspondence, contracts, agreements

Retention begins from the end of the year in which the document was created.

Costs of Full Accounting

Typical monthly accounting costs:

| Company Size | Monthly Cost Range |

|---|---|

| Micro (< 500k PLN revenue) | 500–1,000 PLN |

| Small (500k–2M PLN) | 1,000–2,000 PLN |

| Medium (2M–10M PLN) | 2,000–5,000 PLN |

| Large (>10M PLN) | 5,000+ PLN |

Additional costs:

- Audit: 5,000–30,000 PLN annually (depends on size)

- Software: 100–500 PLN monthly

- Consultations: 200–500 PLN per hour

Frequently Asked Questions

Can a small limited company avoid full accounting?

No. All Sp. z o.o. companies are required to maintain full accounting, regardless of size or revenue.

What if books are not closed by March 31?

Late closing incurs penalties from the tax authority. The company remains liable for all tax filings on deadline despite incomplete books.

Can I do full accounting myself without an accountant?

Technically yes, but it's complex and error-prone. Most companies hire an accountant or use accounting software. Errors can result in tax penalties and audit findings.

Tomasz's 22 years of audit and accounting expertise help companies comply with full accounting requirements and optimize financial processes.